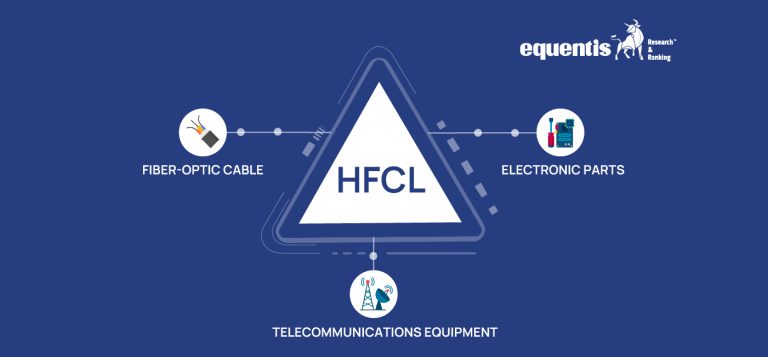

Himachal Futuristic Communications Limited (HFCL) is a leading optical fibre cable manufacturer in India and its recent foray into defence manufacturing has attracted many investors’ interest. HFCL share price, a small cap stock, has also surged in the last five years, and has multiplied investors’ wealth by over 10 times.